Money | U.S. | War Terrorism & Unrest

US equity futures trading with modest gains; UK Budget looms – Newsquawk US Market Open

1 hour ago

Originally posted by: Zero Hedge

- US President Trump thinks they are getting very close to a deal on Ukraine, while he separately commented that they are making progress and Ukraine is happy.

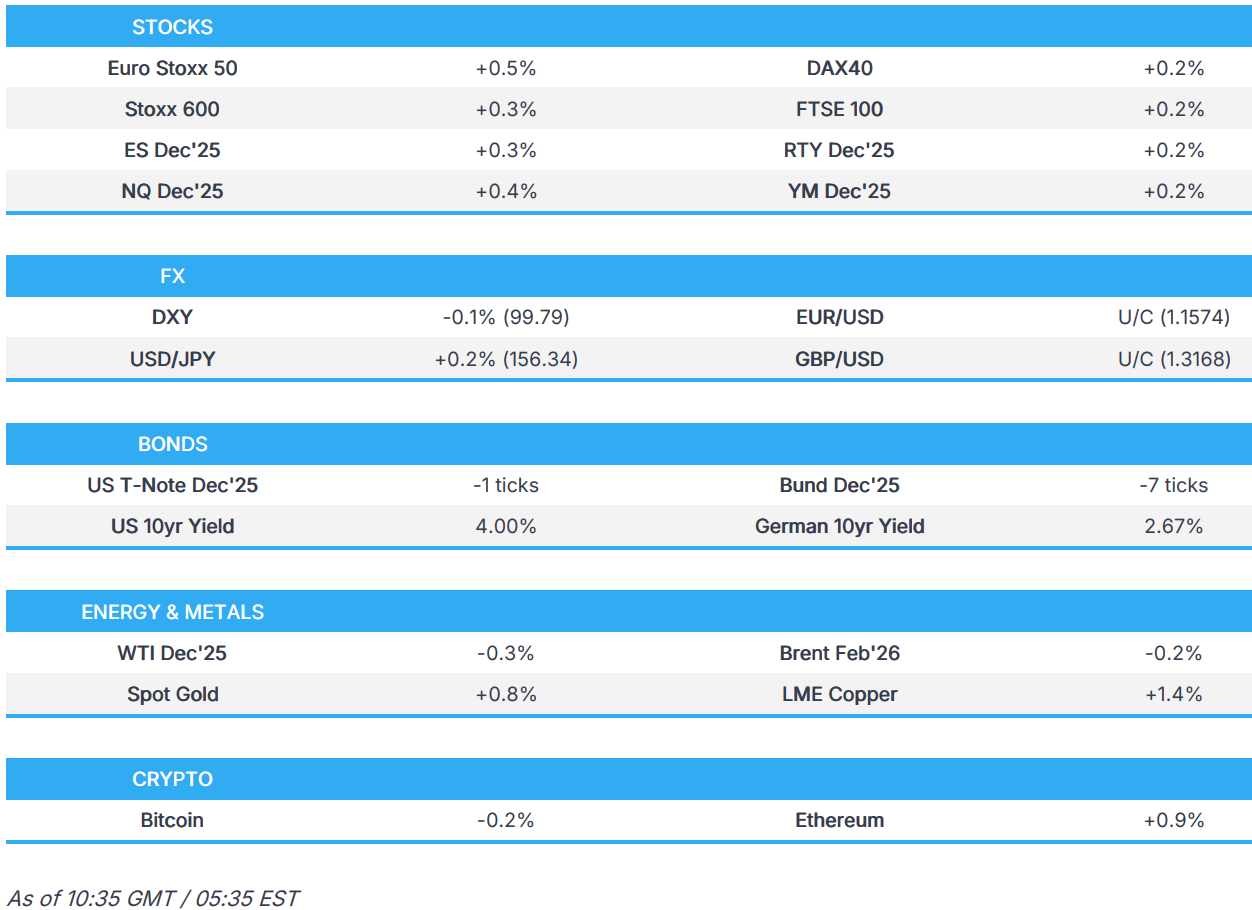

- European bourses are entirely in the green, with the FTSE 100 (+0.2%) trading cautiously ahead of the UK Autumn Budget; US equity futures are modestly firmer.

- DXY is essentially flat, NZD outperforms after the RBNZ cut rates by 25bps (as expected), but projections suggest a pause throughout 2026.

- JPY initially strengthened on reports that the BoJ is preparing markets for a possible hike as soon as December, although one of the sources noted that the decision between hiking in December or January remained a close call; JPY is now lower vs USD.

- Bonds are on the backfoot, paring recent upside; Gilts initially lagged, but now trading in-line with peers as traders eye Chancellor Reeves.

- Crude is a little lower as focus remains on Russia/Ukraine peace talks, 3M LME Copper surges.

- Looking ahead, highlights include US Dallas Fed (Oct), Jobless Claims (w/e 22 Nov), UK Autumn Budget, Fed Beige Book, Speakers including ECB’s Lane & Lagarde, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

TARIFFS/TRADE

- China bought at least 10 cargoes of US soybeans for January shipments, according to traders cited by Reuters.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) opened stronger across the board, continuing the strength seen in APAC overnight; indices slipped a touch off best levels soon after the cash open, before recently bouncing back towards earlier highs. The FTSE 100 (+0.2%) a little more subdued vs peers, ahead of the UK Autumn Budget.

- European sectors hold a slight positive bias; Healthcare tops the pile, buoyed after the US cuts prices Medicare spending on 15 high-priced medicines, by 36%. To the bottom resides Autos and Chemicals.

- US equity futures (ES +0.3%, NQ +0.4% RTY +0.2%) are trading modestly firmer across the board, continuing the gains seen in the prior session – upside today also partly thanks to continued geopolitical progress between Ukraine and Russia.

- Click for the European Equity News

- Click for the Additional European Equity News

FX

- DXY resides in a narrow 99.60-99.87 range at the time of writing after briefly dipping under Tuesday’s 99.65 trough heading into the European open. The index’s upside is limited by gains in EUR amid ongoing constructive headlines surrounding Russia-Ukraine, while it was also reported by Bloomberg that NEC Director Hassett, a close ally of Trump, is the frontrunner for the Fed Chair role, although Fox Business sources refuted the claim. Later today are Jobless Claims, Chicago PMIs and the Fed’s Beige Book.

- EUR is a little firmer/flat vs USD. The single currency found resistance near the 19th of Nov high (1.1597) to trade in a current 1.1563-1.1596 parameter. Focus for EUR traders resides on the Russia-Ukraine peace talks. US President Trump said he thinks that they are getting very close to a deal on Ukraine, while he separately commented that they are making progress and Ukraine is happy. Trump also said Europe will be largely involved in security guarantees. That being said, Russia is expected to reject the new 19-point cease-fire deal drafted by the US and Ukraine, according to NY Post.

- GBP/USD is among the better performers, within a 1.3157-1.3198 band ahead of Chancellor Reeve’s Autumn budget, slated for around 12:30GMT (full Newsquawk preview available on the Research Suite), where market reaction will be contingent on: adherence to fiscal rules, size of headroom, tax combination selected & confidence in the revenue generation, inflation implications of taxes, degree of fiscal tightening, DMO remit, OBR forecasts and finally the implications for the BoE.

- JPY trades on a softer footing, with USD/JPY testing 156.50 to the upside (vs 155.66 low) amid the risk appetite and despite the hawkish-leaning BoJ sources overnight. BoJ is reportedly preparing markets for a possible hike as soon as December, although one of the sources noted that the decision between hiking in December or January remained a close call. Furthermore, Japanese PM Takaichi said the stimulus package isn’t reckless spending and they will watch FX for any speculative moves, and will watch Yen and JGB yields closely.

- NZD/USD outperforms after the RBNZ policy announcement in which the central bank cut the OCR by 25bps to 2.25%, as expected, and kept its options open on future policy, although its projections suggested a pause in rates throughout 2026. The decision saw AUD/NZD slump from 1.1518 to a 1.1407 trough.

- PBoC set USD/CNY mid-point at 7.0796 vs exp. 7.0825 (Prev. 7.0826)

FIXED INCOME

- USTs are trading marginally lower by only a couple of ticks, in quiet and rangebound trade. Focus recently for benchmarks have been on Bloomberg reports that WH NEC Director Hasset is the “frontrunner” to become the next Fed Chair – although this was later refuted by other sources. The implication of such an appointment would be a dovish Fed in the near-term, but with concerns over long-term inflation control in the long-term; a point which has been reflected in yields recently, where a steepening was seen. But overnight that move has reversed a touch, with shorter-term yields outperforming vs longer-term.

- Bunds are also lower by around 10 ticks. Benchmarks saw some early morning pressure, before then reversing back above the 129.00 mark – a move which lacked catalysts; currently trading in a 128.93 to 129.10 range. Really not much from a European perspective, but with focus on geopolitical developments. US President Trump said he thinks that they are getting very close to a deal on Ukraine, while he separately commented that they are making progress and Ukraine is happy. Trump also said Europe will be largely involved in security guarantees. That being said, Russia is expected to reject the new 19-point cease-fire deal drafted by the US and Ukraine, according to NY Post. Thereafter, a better than prior German 2035 auction, spurred some upticks in the benchmark to make a fresh peak at 129.10.

- Gilts began in the red by 23 ticks, counting down to the budget. Since the benchmark has trimmed around half of that and is towards the upper-end of 92.49-79 parameters. Reaction to the budget could be prolonged, as markets need to digest the fiscal package (incl. OBR forecasts and DMO remit), monetary implications (BoE Dec. cut over 80% priced, focus on terminal implications) and the political ramifications. The latter point could take several days to fully emerge, with particular reference to the Labour Left after recent reports that they have the 80 MPs needed to start a leadership challenge, but crucially had not (as of last week, at least) coalesced on an alternate candidate.

- Germany sells EUR 2.344bln vs exp. EUR 3bln 2.60% 2035 Bund: b/c 2.0x (prev. 1.3x), average yield 2.67% (prev. 2.62%), retention 21.87% (prev. 24.93%)

COMMODITIES

- WTI and Brent oscillate in a USD 57.68-58.30/bbl and USD 61.54-62.17/bbl band, respectively, bouncing from a trough of USD 57.10/bbl and USD 60.96/bbl in Tuesday’s US cash session. Focus been on geopols, with early morning commentary via Russia’s Kremlin suggested that it is too early to say if a Ukraine peace deal is close.

- Spot XAU continues to trade beyond Tuesday’s high of USD 4159/oz, aided by the weaker dollar and as Bloomberg reported that White House NAC Director Hassett is the frontrunner for the Fed Chair role. XAU rose at the start of the APAC session from USD 4134/oz to a peak of USD 4169/oz. As the European session gets underway, the yellow metal continues to meander in a USD 4147-4169/oz band.

- 3M LME Copper continues to bid higher throughout the European session, following on from gains in the APAC session, as the global risk tone remains positive and a weaker dollar helps support the metal. After opening at USD 10.87k/t, 3M LME Copper is steadily moving higher and is currently trading at session highs at USD 10.92k/t.

- Deutsche Bank upgrades its 2026 gold forecast to USD 4450/oz (prev. USD 4000/oz). 2026 yearly range of USD 3950-4950/oz.

NOTABLE DATA RECAP

- Swiss Investor Sentiment (Nov) 12.2 (Prev. -7.7)

- Norwegian GDP Growth Mainland (Q3) 0.1% vs. Exp. 0.2% (Prev. 0.6%); GDP Growth (Q3) 1.1% (Prev. 0.8%)

NOTABLE EUROPEAN HEADLINES

- European Commission President von der Leyen will reference language around using frozen Russian assets for a reparations loan to Ukraine, but there won’t be any new announcement on this, via Politico citing sources; in a speech from 08:00BST

- ECB’s Vujcic says he currently sees no reason for a further interest rate cut; ” However, the situation could change if an AI bubble were to burst”, via Borsen Zeitung.

- ECB’s de Guindos says the issue of Fed Swap Lines has not been discussed, no new information.

NOTABLE US HEADLINES

- White House said President Trump is not considering a straight two-year subsidy extension and will make recommendations for healthcare policy improvements soon, while Trump later commented that he doesn’t want to extend subsidies regarding healthcare policy.

- US President Trump was reportedly weighing ousting FBI Director Kash Patel, although Trump later stated that Kash Patel is doing a great job.

GEOPOLITICS

RUSSIA-UKRAINE

- US President Trump thinks they are getting very close to a deal on Ukraine, while he separately commented that they are making progress and Ukraine is happy. Trump said Europe will be largely involved in security guarantees and that the initial 28-point plan was just a map, as well as noted that Special Envoy Witkoff will be meeting with Russian President Putin in Moscow next week. Trump also commented that the Russians are making concessions and there is no deadline for a deal.

- Ukrainian President Zelensky’s Chief of Staff Yermak spoke to US Army Secretary Driscoll and expects him to visit Kyiv this week, while Yermak thanked Driscoll for his objectivity and concrete approach. Furthermore, he said Ukraine is willing to work quickly to finalise steps to end the bloodshed and that Geneva talks on a peace accord provided a good base, with President Zelensky fully ready to work further.

- Russia’s Kremlin Aide Ushakov says Russia has received ‘latest versions’ of US peace plan on Ukraine via the RIA. Says he plans to talk about the leaked conversation during a phone call with US Special Envoy Witkoff, via TASS.

- “Russian presidential aide: Some points in the US plan on Ukraine are positive, but some items in it require discussion”, via Al Jazeera.

- Russia’s Kremlin Spokesperson Peskov urged not to make premature conclusions about the conflict in Ukraine nearing its end.

OTHER

- Taiwan’s President Lai said his government will introduce a historic USD 40bln supplementary defence budget and that the package will not only fund significant new arms acquisitions from the US, but also vastly enhance Taiwan’s asymmetrical capabilities. Lai said Beijing has been trying to turn democratic Taiwan into China’s Taiwan and that China’s threats to the Indo-Pacific are intensifying, while he added that Beijing continues to increase military drills and grey-zone harassment near Taiwan. Lai also stated that China’s infiltration and influence campaigns in Taiwan are intensifying, and China is speeding up military preparations to take Taiwan by force. Furthermore, he said mechanisms will be set up to counter China’s transnational repression and to protect Taiwan’s citizens, as well as noted that “one country, two systems” is a red line for Taiwan and Taiwan will adopt a strategy of self-defence to counter China’s threats.

- Taiwan’s Defence Minister said China has changed its patterns and is squeezing Taiwan’s response time, while he commented that the special defence budget runs from 2026 to 2033 and will cover items from missiles to drones to counter fast-rising Chinese threats.

- US de facto ambassador to Taiwan welcomes President Lai’s announcement of a new special defence budget and said the US supports Taiwan’s rapid acquisition of critical asymmetric capabilities needed to strengthen deterrence, while he stated that today’s announcement is a major step toward maintaining peace and stability across the Taiwan Strait by strengthening deterrence.

- China’s Taiwan Affairs Office said regarding Japan’s missile deployment plan near Taiwan, that they have firm will, strong determination and a powerful ability to crush all foreign interference schemes.

- Cuba’s Foreign Minister said US intervention in Venezuela would be a violation of international law and the UN Charter, while he added that the exaggerated and aggressive military presence of the US in the region constitutes a threat against Latin America and the Caribbean as a whole.

CRYPTO

- Bitcoin is a little lower and trades just under the USD 87k, whilst Ethereum climbs back above USD 2.9k.

APAC TRADE

- APAC stocks mostly followed suit to the gains on Wall Street, where stocks were underpinned amid Russia/Ukraine optimism and a softer yield environment.

- ASX 200 was led higher by outperformance in mining and materials, with most sectors in the green aside from utilities, tech and telecoms.

- Nikkei 225 rallied with SoftBank among the biggest gainers as it rebounded from the previous day’s OpenAI-related slump, and with participants shrugging off a source report that the BoJ is preparing markets for a possible hike as soon as December, although one of the sources noted that the decision between hiking in December or January remained a close call.

- Hang Seng and Shanghai Comp lagged amid a focus on earnings with mixed results from the likes of Alibaba and NIO.

- US equity futures marginally extended on the previous day’s advances heading into the Thanksgiving holiday weekend.

NOTABLE ASIA-PAC HEADLINES

- BoJ is said to be preparing markets for a possible interest rate hike as soon as December with a tweak to communication, according to Reuters sources, although one of the sources said the decision on whether to hike in December or hold off until January remains a close call.

- RBNZ cut the OCR by 25bps to 2.25%, as expected, and stated that future moves in the OCR will depend on the outlook for the medium-term. RBNZ said annual consumer inflation increased to 3% in the September quarter but added that with spare capacity in the economy, inflation is expected to fall to around 2% by mid-2026, while it commented that risks to the inflation outlook are balanced and economic activity was weak over mid-2025 but is picking up. Furthermore, it projected the Official Cash Rate at 2.25% in March 2026 (prev. 2.55%) and at 2.28% in December 2026 (prev. 2.62%). RBNZ Minutes revealed that the decision was made by a vote of 5-1 and that the committee discussed the options of holding the OCR at 2.50% or lowering it to 2.25% in which the case for a hold emphasised the considerable reduction in the OCR to date, while the case for a cut emphasised significant excess capacity in the economy.

- Japanese PM Takaichi said the stimulus package isn’t reckless spending, and added that a strengthening economy can help improve Japan’s fiscal health. She said JGB issuance for this fiscal year will be below last year’s size, including expected issuance for extra budget, and it is important to ensure fiscal sustainability. She noted they will strike to lower debt-to-GDP ratio with a close eye on interest rates, and the government will take appropriate steps by gauging whether FX rates reflect fundamentals. She said they will watch FX for any speculative moves, and will watch Yen and JGB yields closely.

- RBNZ Governor Hawkesby said he feels that risks are balanced and they are in a great position to mitigate risks, while he stated the central projection is based on the Cash Rate being on hold through 2026, as well as noted that economic indicators are picking up across all high-frequency measures and the current cash rate is supportive and stimulatory. Hawkesby also commented that they retain full optionality on the cash rate with every option on the table.

- Japan is to reportedly issue more than JPY 11tln in additional government bonds for FY25 extra budget, according to TV Asahi

- US and Taiwan target trade and investment deal which includes training for American workforce, according to Reuters citing sources

DATA RECAP

- Japanese Services PPI (Oct) 2.70% vs. Exp. 2.70% (Prev. 3.00%)

- Australian CPI YY (Oct) 3.80% vs. Exp. 3.60%

- Australian Weighted Median CPI YY SA (Oct) 3.40% vs. Exp. 2.95%

- Australian Trimmed Mean CPI YY SA (Oct) 3.3% vs. Exp. 3.0%

- Australian Construction Work Done (Q3) -0.7% vs. Exp. 0.4% (Prev. 3.0%)

Loading…

Recent Top Stories

Sorry, we couldn't find any posts. Please try a different search.