Futures Rise With Trump Tariff Updates, FOMC Minutes On Deck

US equity futures inch higher as the market tries to regain some losses a day after President Donald Trump escalated his trade rhetoric and threatened more charges on copper and pharmaceuticals. Trump also foreshadowed an update to the trade status, saying he “will be releasing a minimum of 7 Countries having to do with trade” on Wednesday morning and with an additional number of countries to be released in the afternoon as we reach the 90-day deadline to Liberation Day. As of 8:00am, S&P and Nasdaq futures are 0.2% higher, with Mag7 names trading higher premarket while semis are mixed; banks and industrials are boosting cyclicals. Europe is also trending higher (+80bps) for a third day, while Asia finished mostly lower (HSI -1%, with HS Tech -1.7%). Goldman writes that heavy focus on recent momentum unwind (the Goldman High Beta Momentum Pair Basket -4.5% yesterday and now down 8.3% mtd). Recent catalysts for the Momo Reversal seem to be: the move in back-end Rates / positioning / ongoing re-shuffling to start the quarter / and the big reversal lower in Banks yesterday. Elsewhere, some minor underperformance in haven assets suggests investors are not too concerned by what Trump may reveal later today. Spot gold loses $10 or so. Treasuries are steady with bond yields flat to up 1bp as the USD is indicated higher. Commodities are also higher in both Ags/Energy as metals are generally weaker post-copper tariff announcement. Trump’s 50% copper tariffs would be “extremely inflationary,” according to UBS O’Connor Global Multi-Strategy Alpha CIO Bernie Ahkong, while Goldman Sachs expects inbound-US flows of the metal to accelerate as the incentive to “front-run” the tariff implementation has increased. Today’s macro data focus is on Fed Minutes, mtge applications, and inventories.

In premarket trading, Microsoft gains 0.8% after Oppenheimer raised the recommendation on the software company to outperform, citing potential upside as AI revenue grows quickly and “investors embrace Microsoft as one of the long-term AI winners in software.” Other Mag7 names are all higher (Tesla +0.5%, Amazon +0.3%, Meta +0.3%, Nvidia +0.2%, Alphabet +0.3%, Apple unch).

- Aehr Test Systems (AEHR) drops 20% after the maker of semiconductor equipment posted fiscal 4Q revenue that slipped from the year-ago period.

- AES Corp. (AES) is exploring options including a potential sale amid takeover interest, according to people familiar. Shares are up 14%.

- Bloom Energy (BE) gains 7% as JPMorgan upgraded its rating to overweight after fuel cells unexpectedly qualified for Clean Electricity Investment credits as part of the new tax bill.

- Doximity Inc. (DOCS) rises 3% after Evercore ISI upgraded the healthcare-software company to outperform, saying the fiscal 2026 guidance is conservative.

- Mobileye Global (MBLY) slips 1.2% after the maker of software and hardware technology for automobiles announced a secondary offering by Intel. It also reported preliminary second-quarter results that beat expectations. Intel shares are down 0.9% premarket.

- RxSight (RXST) tumbles 40% after the company cut its 2025 revenue forecast and reported preliminary second-quarter revenue that fell short of Wall Street’s expectations.

- Starbucks Corp. has received proposals from prospective investors in its China business, most of whom are eyeing a controlling stake in the operation, said people familiar with the matter. Shares are up 1.7%.

- Tandem Diabetes (TNDM) declines 4% after Citi downgraded the medical device maker to sell from neutral, citing a series of headwinds including competition pressures.

- T-Mobile (TMUS) drops 1.9% as KeyBanc Capital Markets cuts to underweight, saying the telecom company’s stock underperformance is set to continue and that its “premium valuation is just too high.”

In corporate news, there was another round of street actions moving stocks early (MSFT upgraded @ Oppenheimer / SMCI downgraded @ BofA / TMUS downgraded @ Keybanc). Elsewhere, Apple’s COO and company veteran Jeff Williams is stepping down this month before retiring later in the year. The firm is also said to be in talks to acquire the US rights to screen Formula 1 after the success of its hit movie, according to the FT. META is investing $3.5bn in a AI Glasses company; BABA is trading -2.5% after JD.com announced a new food delivery company; bloomberg is reporting that China wants to use 115,000 banned NVDA chips to fulfill its AI Ambitions; and SpaceX is said to be planning an offering valuing the company at $400bn (only 19 publicly traded companies in the S&P have a large mkt cap). Intel is selling 45 million shares of Mobileye, in a move seen likely to support Intel’s near-term liquidity and cash needs as it funds foundry ambitions, according to Bloomberg Intelligence.

Investors will seek clues for more insight on Fed’s policy path when the latest FOMC meeting minutes are released later today, amid increasing pressure on Powell from Trump. Kevin Hassett and Kevin Warsh are vying to be the next Fed chair, according to the WSJ.

Earlier this week, traders had largely brushed off a batch of letters in which Trump effectively delayed his tariff deadline while outlining new rates targeting over a dozen countries. Sentiment shifted on Tuesday, when he signaled fresh resolve to move forward with steep levies on foreign imports. He also signaled that updates to the trade status of at least seven nations would be released Wednesday morning, with more announcements later in the day.

“The market has already overreacted in the past on Trump’s trade announcements, so I think investors are being prudent and cautious,” said Stéphane Deo, senior portfolio manager at Eleva Capital in Paris. “That being said, tariffs will end up being much higher in the fall than they were at the beginning of the year, so that’s likely to fuel inflation.”

Investors will also parse minutes of the Federal Reserve’s June policy meeting later today for indications on whether officials are closer to lowering interest rates. Trump accused Fed Chair Jerome Powell of “whining like a baby about non-existent inflation” as he intensified his standoff over the pause in rate cuts. Swaps are almost fully pricing two quarter-point cuts until the end of the year, with a 65% chance of a first reduction in September.

Europe’s Stoxx 600 is up 0.8% and set to rise for the third consecutive session, to the highest in almost a month, as investors look for signs of progress in trade negotiations with the US. Bank and energy names are leading gains while media shares provide a drag. Miners underperform after President Donald Trump indicated the US would implement a higher-than-expected 50% tariff on copper imports. Here are the biggest movers Wednesday:

- EssilorLuxottica shares rise as much as 5.5%, the most in three months, after Facebook parent Meta acquired just under 3% of the Ray-Ban maker, according to people familiar with the matter

- British American Tobacco shares rise as much as 2.9%, the most in over a month, after Jefferies named the firm as its top pick as it reinstated coverage of the global tobacco sector

- Renk shares rise as much as 5.9%, the most since June, after Bloomberg reported the German gearbox maker is considering options for its civilian industrial business as it looks to focus on defense operations

- Indra Sistemas rises as much as 4% in Madrid as Goldman Sachs raises its recommendation to buy from neutral, noting the firm is a beneficiary of the “defense mega trend”

- Hunting shares rise as much as 15%, the most since May 2024, after the British engineering group announced an increase in targeted dividend distributions in its H1 trade results and proposed a $40m share buyback

- Santam shares rise as much as 4.3% in Johannesburg, to a record high, after JPMorgan increased its price target on the short-term insurer to a new Street high of 527.71 rand from 480 rand

- WPP shares drop as much as 16%, to the lowest since 2009, after the advertising agency reduced its organic growth guidance for the year, citing continued macro uncertainty that weighed on client spending

- Kongsberg falls as much as 7.6% as DNB Carnegie says soft second quarter results could bring down consensus estimates, even as company cites “substantial” demand for its defense systems

- FDJ United shares tumble as much as 5.2%, falling for a fifth consecutive session to their lowest level since April, after a unit of Credit Agricole sold its entire stake in the lottery and sports-betting firm at a discount

- Inwido falls as much as 6.2%, the most since April, after DNB Carnegie cut its recommendation on the Swedish window and door manufacturer to hold, saying the shares are fairly valued after a good run

- Close Brothers tumbles as much as 9.1%, pulling back after reaching an eight-month high, as the firm warned a revamp of its premium finance business will cause the unit’s loan book to decline

- Zigup shares fall as much as 8.2% after the UK-based rental firm reported lower profits on vehicle disposals in preliminary FY25 earnings. Panmure Liberum says this risks eroding the group’s profits in the future

Earlier in the session, Asian stocks fell as investor mood soured following US President Donald Trump’s latest vow to push forward with his aggressive tariff agenda. The MSCI Asia Pacific Index lost as much as 0.4%, with Alibaba, Tencent and Samsung Electronics among the biggest drags. Equities in Hong Kong were among the top losers in the region, partly weighed by declines in metals stocks. Copper names including Zijin Mining fell after Trump said he planned to implement a 50% tariff on imports of the commodity. Shares in Australia and New Zealand also fell after Trump’s tariff announcements from the White House. The Reserve Bank of New Zealand decided to leave interest rates unchanged, as expected. Malaysia’s stock benchmark index was down about 0.4% as the central bank cut its interest rate for the first time since 2020 amid trade tensions.

In FX, the dollar swung between gains and losses and stayed in tight ranges versus its major peers, while options pointed to demand for bullish exposure. The Canadian dollar underperforms slightly with a 0.2% fall.

- USD/JPY -0.1% to 146.73 (range 146.53 – 147.18)

- EUR/USD little changed at 1.1721 (range 1.1702 – 1.1729)

- GBP/USD little changed at 1.3599 (range 1.3565 – 1.3606)

In rates, treasuries drop, with US 10-year yields rising 2bps to 4.42% following a five-day run of losses which lifted the rate almost 20 basis points. The Treasury will sell $39 billion of 10-year notes later Wednesday followed by $22 billion of 30-year bonds Thursday. An offering of three-year securities on Tuesday was met with soft demand. Bunds edge higher with German 10-year borrowing costs down 1 bp at 2.68%. The Gilt curve flattens as short-end maturities underperform and lag gains at the longer-end.

“This week’s Treasury auctions are going to be important, at least in the short term, particularly where we are in terms of the tax cut extensions and the tariff negotiations,” said Justin Onuekwusi, chief investment officer at St James’s Place in London.

In commodities, oil prices advance, with WTI up 0.5% at $68.70 a barrel; spot gold falls $12 to around $3,290/oz. Bitcoin trades in a narrow range as we await further tariffs updates later in the session. At best, still just under 1k from the in-focus USD 110k mark.

Looking at today’s calendar, the US economic data slate includes May wholesale inventories (10am) and minutes of the June FOMC meeting (2pm). Fed speaker slate is blank

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.2%

- Russell 2000 mini little changed

- Stoxx Europe 600 +0.7%

- DAX +1%

- CAC 40 +1.2%

- 10-year Treasury yield -1 basis point at 4.39%

- VIX -0.5 points at 16.33

- Bloomberg Dollar Index little changed at 1196.96

- euro -0.1% at $1.1712

- WTI crude +0.5% at $68.67/barrel

Top Overnight news

- President Donald Trump vowed to push forward with his aggressive tariff regime in the coming days, stressing he would not offer additional extensions on country-specific levies set to now hit in early August while indicating he could announce substantial new rates on imports of copper and pharmaceuticals.

- White House NEC Director Kevin Hassett has emerged as a contender for the next Fed Chair in a possible threat to early favourite Kevin Warsh and has met with President Trump at least twice in June regarding the job, according to WSJ.

- US Speaker Johnson, when asked on government funding state of play, said “We want to appropriate at lower levels. We just have to determine what those levels are exactly”, via Punchbowl.

- Copper futures fell in London after President Donald Trump sowed chaos in metals markets by indicating the US would implement a higher-than-expected 50% tariff on imports of the commodity.

- Meta Platforms Inc. bought a minority stake in the world’s largest eyewear manufacturer, EssilorLuxottica SA, deepening the US tech giant’s commitment to the fast-growing smart glasses industry, according to people familiar with the matter.

- Active investment managers have no option but to adopt hedge fund strategies to counter the migration to low-cost passively run portfolios, according to an outperforming French asset manager.

- DoJ said to be investing UnitedHealth’s (UNH) Medicare billing, according to WSJ sources.

Trade/Tariffs

- US President Trump delayed reciprocal tariffs as Treasury Secretary Bessent wanted more time on deals, according to WSJ.

- US President Trump posted they “will be releasing a minimum of 7 Countries having to do with trade” on Wednesday morning and with an additional number of countries to be released in the afternoon.

- EU negotiators are closing in on a trade deal with US President Trump that would leave the EU facing higher tariffs than the UK, with the EU not expecting to achieve the same access to the US market as British steel, cars and other products subject to sectoral duties. Furthermore, Brussels is ready to sign a temporary “framework” agreement that sets Trump’s “reciprocal” tariff at 10% while talks continue, according to FT.

- China’s Commerce Ministry placed eight Taiwanese companies on its export control list due to concerns regarding dual-use technologies.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following the similar performance stateside where tariff updates remained in focus after the US flagged more tariff letters and President Trump suggested a 50% tariff on copper. ASX 200 marginally retreated with most sectors in the red although price action was confined within tight parameters. Nikkei 225 swung between gains and losses amid global trade uncertainty, while there were balanced comments from BoJ’s Koeda who stated it is inappropriate to say the specific timing of the next rate hike now due to high uncertainty but added the BoJ must debate how much it should eventually shrink its expanded balance sheet and balance of JGB holdings. Hang Seng and Shanghai Comp conformed to the mixed overall picture in the region as property names dragged the Hong Kong benchmark lower, while the mainland remained afloat as participants reflected on mixed inflation data from China.

Top Asian News

- China’s state planner chair said to expect the size of China’s economy to exceed CNY 140tln this year and noted that foreign tech curbs can only strengthen China’s tech innovation and resolve on self-reliance.

- BoJ’s Koeda said recent rises in Japan’s food and rice prices were stronger than expected at the time of BoJ’s May policy meeting and they are watching the development carefully, while he added the BoJ’s weighted median inflation is still below 2% and must scrutinise whether momentum for stable inflation is becoming embedded in Japan’s economy. Koeda also commented that it is inappropriate to say the specific timing of the next rate hike now due to high uncertainty over the economic outlook and stated the BoJ must debate how much it should eventually shrink its expanded balance sheet and balance of JGB holdings.

- ex-BoJ policymaker Sakurai says BoJ will hold off rate hikes until March due to the US tariffs, according to Reuters.

- RBNZ kept the OCR at 3.25%, as expected, while it stated that if medium-term inflation pressures continue to ease as projected, the Committee expects to lower the OCR further and annual consumer price inflation will likely increase towards the top of the Monetary Policy Committee’s 1-3% target band over mid-2025. RBNZ stated the economic outlook remains highly uncertain and further data on the speed of New Zealand’s economic recovery, the persistence of inflation, and the impacts of tariffs will influence the future path of the OCR. The minutes from the meeting stated the Committee expects to lower the official cash rate further, broadly consistent with the projection outlined in May and the case for keeping the OCR on hold at this meeting highlighted the elevated level of uncertainty and the benefits of waiting until August in light of near-term inflation risks. Furthermore, the Committee discussed the options of cutting the OCR by 25bps or keeping the OCR on hold at this meeting and some members emphasised that further monetary easing in July would provide a guardrail to ensure the recovery of economic activity.

- China State Council issues notice on stepping up support for employment, via Xinhua; will support enterprises in stabilising jobs; will expand the scope of social insurance subsidies. To further enrich the policy toolkit in order to stabilise employment.

European bourses began the day with modest gains and have been grinding higher throughout the morning, Euro Stoxx 50 +1.1%; strength comes with the EU said to be nearing a deal with the US, with modest outperformance in the DAX 40 +1.2% amid associated auto strength. Amidst this, sectors began mixed but have been moving toward an overall positive bias. Banks lead with UniCredit (+3%) raising its stake in Commerzbank (+1%). Basic Resources weaker given pressure in non-US copper, hitting London-based minders, while Media lags after WPP’s (-17%) profit warning.

Top European News

- BoE Financial Stability Report – July 2025; maintains CCyB at 2%. Uncertainty around the global risk outlook remains materially elevated compared to the time of the November FSR. Bank plans to engage with industry through an upcoming discussion paper, which will seek views on potential options to help mitigate gilt repo market vulnerabilities.

- BoE’s Bailey (at the FSR) says risks and uncertainty still elevated. UK borrowers are resilient and can be supported by banks. Steepening in yield curves is not particularly UK-focused. Steepening in yield curves will need to be looked at carefully when it comes to the QT decision. QT is an open decision.

- Union confirms that UK Junior Doctors will go on strike between July 25-30th.

FX

- USD steady as markets digest Tuesday’s trade updates and await another batch later today. DXY contained in a 97.49-72 band. Amidst this, G10 peers are slightly mixed vs the USD but are broadly contained thus far.

- GBP the marginal best performer, Cable to a 1.3608 peak at best but hasn’t spent much time above the figure in 1.3565-1.3608 confines. No reaction to the FSR and as trade updates for the UK are expected to be light, the USD-side of the equation will likely do the heavy lifting for today.

- EUR marginally softer vs the USD, EUR/USD holding just above 1.17 in a 1.1702-29 confine, and well within yesterday’s 1.1682-1.1765 parameter. Specifics light thus far as we await updates on trade, after Trump said a letter was two days away which means a deal. Ahead, a handful of ECB speakers.

- Antipodeans relatively contained, particularly when compared to the RBA-led outperformance in the AUD earlier in the week. AUD/USD currently holding around highs of 0.6544, but essentially flat. Overnight, the RBNZ was unchanged as expected but guided towards further cuts if data moves as projected, essentially taking a data-dependent approach; as such,Kiwi is flat at 0.6000 vs the USD.

- JPY softer. We continue to await updates on the US-Japanese trade front with rhetoric earlier in the week not indicative of a near-term breakthrough. That aside, the firmer risk tone this morning has potentially been exerting some modest pressure. However, despite the continued improvement in the risk tone, USD/JPY is off overnight highs above 147.00, closer to a 146.54 trough.

- PBoC set USD/CNY mid-point at 7.1541 vs exp. 7.1806 (Prev. 7.1534).

Fixed Income

- A modest upward bias for benchmarks after a few sessions of relatively marked pressure.

- Strength comes despite the constructive risk tone. But, the magnitude of today’s move is limited in nature with Bunds for instance still lower by over 60 ticks WTD, and the move more a function of Bunds retracing some of Tuesday’s supply-induced pressure (primarily from EU debt) than a pronounced move higher.

- No move in EGBs to the day’s dual-tranche Bund supply. Now awaiting ECB speak and potential comments from the German Chancellor in a Bundestag Q&A on the draft 2026 budget.

- USTs a similar story with specifics light into supply and FOMC Minutes. Thus far, confined to a 110-24 to 110-29+ band, within Tuesday’s slightly more expansive 110-21+ to 111-01+ parameters, and by extension shy of Monday’s 111-12+ WTD peak.

- Gilts in-fitting with USTs and EGBs. Firmer by a handful of ticks with newsflow light as the UK has already secured a trade deal. Off best, but still firmer, in a 91.63-83 band; as is the case for USTs and Bunds remains shy of peaks at 91.98 and 92.63 from the last two sessions.

- UK sells GBP 4.5bln 4.50% 2035 Gilt: b/c 2.89x (prev. 2.98x), average yield 4.635% (prev. 4.588%) & tail 0.2bps (prev. 0.3bps)

- Germany sells EUR 1.135bln vs exp. EUR 1.5bln 2.60% 2041 and EUR 0.794bln vs exp. EUR 1.0bln 2.50% 2044 Bund

Commodities

- Upward bias across the crude contracts with Brent front-month settling north of USD 70/bbl yesterday following the OPEC+ surprise over the weekend, in the form of a larger-than-expected supply increase for August.

- WTI resides in a USD 67.78-68.94/bbl range while its Brent counterpart trades in a USD 69.85-70.71/bbl range.

- Softer trade across precious metals despite a relatively stable Dollar. Weakness in the complex could be a function of optimism regarding trade deals. Spot gold continues yesterday’s weakness and resides in a USD 3,282.66-3,308.15/oz range, with the next point the 30th June trough at USD 3,244.42/oz.

- Base metals are softer, in Europe, despite the commentary from Trump on copper tariffs lifting to 50%. Front-running of US copper ahead of the potential 50% tariff has widened the Comex-LME arbitrage to over USD 2,000/t and pushed Comex inventories above combined LME and SHFE levels, writes ING.

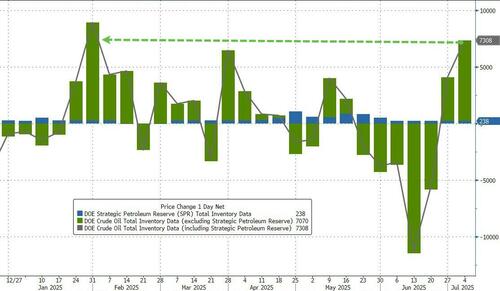

- US Private Inventory Data (bbls): Crude +7.1mln (exp. -2.1mln), Distillate -0.8mln (exp. -0.3mln), Gasoline -2.2mln (exp. -1.5mln), Cushing +0.1mln.

- Mexico’s Economy Minister said he will have a call with US authorities to discuss copper tariffs and see what they apply to.

- UAE Energy Minister says not worried about oil supply overhang, not seen an increase in inventories. Adds, they are losing some of the world’s spare oil capacity Y/Y as some nations cannot produce what they did last year or last month and nobody is talking about peak oil demand anymore, demand has surpassed predictions.

- Goldman Sachs maintains its December 2025 LME Copper price forecast at USD 9.7k. Changes the baseline view on US tariffs on copper imports to 50% (prev. exp. 25%).

- West African cocoa production is likely to see another 10% decline in the upcoming 2025/26 season, according to Reuters citing industry sources.

Geopolitics: Middle East

- US President Trump exerted strong pressure on Israeli PM Netanyahu during their meeting to end the war, according to Yedioth Ahronoth citing informed sources.

- Qatari delegation arrived on Tuesday for talks at the White House regarding the hostage deal and ceasefire in Gaza, according to Axios citing a source familiar.

- IDF presence in Gaza is understood to be the ‘only issue’ still to be resolved in the push for Israel-Hamas ceasefire and the two sides have bridged significant differences on several other issues, according to Sky News citing sources.

- Kann News citing Saudi royal family sources believes that the agreement being formulated between Israel, Syria and the United States could have a positive effect and prepare the ground for an agreement with the Saudis as well.

- US Envoy Witkoff said to have postponed travel to Doha for Israel-Hamas peace talks, according to Times of Israel.

Geopolitics: Ukraine

- White House considers giving Ukraine another Patriot air defence system, according to the Wall Street Journal.

- Ukrainian attack on a beach in the Russian city of Kursk killed three people, according to the regional governor.

- Russia launched a “record” 728 drones overnight and 13 missiles, according to Ukraine’s Air Force.

- German Chancellor Merz says diplomatic means to resolve the Ukraine war have been exhausted.

- Russia’s Kremlin says “we are calm” about US President Trump’s criticism of Russian President Putin. Trump has a tough style in the phrases he uses. Will continue to try to fix the broken Russia-US relationship.

- Ukrainian President Zelensky is due to meet with US Special Envoy Kellogg during his visit to Rome, according to Ifax.

US Event Calendar

- 7:00 am: Jul 4 MBA Mortgage Applications, prior 2.7%

- 10:00 am: May F Wholesale Inventories MoM, est. -0.3%, prior -0.3%

- 2:00 pm: Jun 18 FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Equity markets have been treading water over the last 24 hours, even with the latest tariff developments and some renewed jitters in global bond markets around fiscal sustainability. That meant yields rose in pretty much every major economy, with 10yr Treasury yields (+2.0bps) by no means the worst hit but still rising for a 5th consecutive session, before rising another +1.4bps this morning. Meanwhile, the S&P 500 (-0.07%) edged back for a second day as Trump said there’ll be no further tariff extensions beyond August 1st, with futures down another -0.12% overnight. And it was also a record day for US copper futures after Trump said copper would face 50% tariffs, with the biggest daily jump (+13.25%) in available data back to the late-1980s.

In terms of how the day unfolded, that bond selloff initially began in Japan, where there was a big spike in long-end bond yields that pushed the 30yr yield up +9.0bps, and back above 3%. That’s coming ahead of the upper house election there on July 20, where the major parties are advocating further spending or tax cuts, so that’s adding to concerns at a time when the Bank of Japan are already scaling back their bond purchases. And as we just managed to sneak into yesterday’s edition, the Reserve Bank of Australia voted to keep rates on hold, even though a cut was widely expected, so that helped to push yields higher in Australia too.

That momentum carried over into the European session, where yields moved up across the continent. UK gilts saw the biggest moves, with their 30yr yield (+6.3bps) back up to 5.45%, whilst the 10yr yield was up +4.7bps to 4.63%. So in both cases, that took yields above their close last Wednesday when Chancellor Reeves’ position looked under threat, and investors feared that the government might ease the fiscal rules. Coincidentally, the OBR fiscal watchdog published their “Fiscal risks and sustainability” report yesterday, which concluded that demographic pressures would help push debt-to-GDP above 270% of GDP by the early 2070s, at least on current policy. Admittedly, it’s a similar situation if you look at the CBO’s long-term reports for the US, but it demonstrates how this problem isn’t going away on the current trajectory.

These concerns were clear on both sides of the Atlantic, and 30yr Treasury yields earlier got close to 5% again, closing up +0.9bps at 4.92% after having reached 4.97% in early NY trading. Bear in mind we’ve got a 10yr Treasury auction today and a 30yr auction tomorrow, so those will be in the spotlight to see how much demand there is. Meanwhile in Europe, 10yr bund yields were up +4.4bps to 2.69%, whilst the 30yr yield (+5.4bps) hit 3.17%, which is just shy of its post-Euro crisis peak of 3.21% from late-2023. On the topic of German fiscal policy, DB are hosting a webinar today at 1pm London time on the latest developments and its impact. The details to register can be found here.

Otherwise, trade and tariffs were the main focus yesterday, and the big development was Trump saying that “No extensions will be granted” to the August 1 deadline on the reciprocal tariffs. That’s a shift in tone from Trump’s own comments on Monday evening, as Trump had said that the August 1 date was “not 100% firm”, and investors had been hopeful that ongoing negotiations and trade deals could avoid that. So it’s a clear hardening up of the rhetoric. During a cabinet meeting yesterday, the President took a hard line against the BRICS countries again, saying the group was “set up to hurt us…I can play that game too so anybody that’s in BRICS is getting a 10%” tariff addition. This comes even though he had previously noted that he was close to a deal with India. In addition, the President took a more hawkish tone, indicating that some countries would be seeing a 60% or 70% tariff rate and that sectoral tariffs are coming. While pharma, autos, and steel have been well flagged, the President proposed a 50% rate on copper products and said that some drug levies could reach as high as 200%, although the President stated that the pharma tariffs would only come after a “year or year and half”. Copper first month futures on the NY exchange hit an all-time high in response, as prices rose 13.25% (17% intraday), which was the largest daily move since on record going back to 1988.

Amidst those headlines, there was some more constructive news as we heard that the Japan-US talks were continuing, and Japan’s Ministry of Foreign Affairs said that economic revitalisation minister Ryosei Akazawa had a 30 minute phone call with Treasury Secretary Bessent. In the statement, it said that Japan would “continue to explore ways for a mutually beneficial agreement”, and it was later reported by Bloomberg that Bessent would be in Japan next week for the 2025 World Expo. President Trump indicated that at least seven tariff letters would be coming out this morning, Washington time, with more expected as the week goes on. Ultimately, the “reciprocal” tariffs rates have been extended to August 1st given Monday’s executive order, so investors will continue to weigh how likely the administration is to go through with the higher rates over the next three weeks.

That backdrop meant equities struggled, with the S&P 500 (-0.07%) losing further ground after its decline on Monday. However, the decline wasn’t particularly broad-based, and the equal-weighted S&P 500 was actually up +0.25% on the day. At the sub-sector level, Energy outperformed (+2.7%) on the back of higher oil prices (Brent crude up 0.82% yesterday), while Autos (1.2%), Semiconductors (+1.0%) and Pharma (+0.9%) all outperformed despite the specific sectoral tariff threats. There was also a decent divergence between the megacaps in the Magnificent 7 (-0.07%), and the small-caps in the Russell 2000 (+0.66%). Meanwhile in Europe, the mood was generally more positive, with the STOXX 600 (+0.41%) paring back its earlier losses after the news came through about the US-Japan call.

Overnight in Asia, most equity indices have managed to post an advance, with gains for the Nikkei (+0.18%), the KOSPI (+0.65%), the CSI 300 (+0.32%) and the Shanghai Comp (+0.29%). Indeed, the Shanghai Comp is currently on track to close at its highest level since early 2022. However, there’s been weakness elsewhere, and the Hang Seng is down -0.74%, whilst Australia’s S&P/ASX 200 is down -0.41% after the RBA’s unexpected decision to remain on hold yesterday. Indeed, Australian government bond yields have seen a further jump this morning, with the 10yr yield up another +9.0bps to 4.35%. The Reserve Bank of New Zealand have also kept rates on hold this morning at 3.25%, although that decision was widely expected.

Otherwise, the latest inflation data from China has been released overnight, which showed producer prices were down -3.6% year-on-year (vs. -3.2% expected). That’s a 33rd consecutive month of declining prices, and the biggest rate of decline in 23 months. However, consumer prices unexpectedly rose +0.1% (vs. -0.1% expected), marking the first inflationary reading since January.

There wasn’t much data yesterday, although the NFIB’s small business optimism index came out, which was exactly in line with consensus at 98.6. Otherwise, the New York Fed’s Survey of Consumer Expectations saw little change in inflation expectations. The 1yr measure was down to 3.0% in June, the lowest since January, but the 3yr measure was unchanged at 3.0%, and the 5yr was also unchanged at 2.6%.

To the day ahead now, and we’ll get the minutes from the FOMC’s June meeting, and hear from ECB Vice President de Guindos, and Bundesbank President Nagel. The Bank of England will also release their Financial Stability Report.

Loading…

{kind=link}